The movie industry has changed a lot over the years, mostly because our attention span has shrunk with the invention of the internet and having instant entertainment on our phones at all times. Go back and watch old movies; and they start very slowly and build to the climax. Today, we see the end first, followed by a subtitle that takes us back to the past to find out what led up to the end. Let’s do that with this newsletter! The S&P 500 finished the second quarter at the fifth record close of 2025, up over 10% for the quarter and 5.5% year-to-date. If that was the whole story we would all be happy, on pace for another double-digit gain in the market!

Now let’s go back three months! In our Q1 newsletter (available on our website) discussed Liberation Day which happened April 2. After the S&P 500 was already down 4.6% in the first quarter, the announcement of worldwide tariffs sent the markets reeling down and the VIX (a measure of volatility) skyrocketed to 50. At the time of the newsletter, we had no idea what would happen, but we started that section with “We are NOT recommending that our clients panic at this time and make broad changes to their asset allocations.” We went on to mention that we took advantage of the huge move in the markets to buy stocks and create structured notes, including Callable Yields Notes at 18.95%, 17.50% and 16.25% respectively.

Shortly after our newsletter went out to clients and prospects, President Trump announced a 90-day extension until the tariffs would go into effect, so countries around the world could negotiate. The markets took off, and as we mentioned earlier, finished the quarter at all-time highs.

It is unclear as of now where Liberation Day will fall in history or if it will even be remembered, but for now there is a lasting memory of President Trump and the Reciprocal Tariff board that was presented on the White House lawn. There was a blanket 10% tariff rate on all exporters to the U.S. in addition to higher reciprocal rates on 60 trading partners with larger trade deficits, including China, Japan and the European Union. The market immediately sold off with over 80% of the companies in the S&P 500 down that morning, with two thirds down at least 2%. Companies that relied on overseas manufacturing were down by over 10% that day. The idea of the tariffs is to bring manufacturing back to the U.S. The quick reaction to delay the tariffs for 90 days was probably prompted by the bond market. The U.S. has a very large deficit, and the government wants to see interest rates come down since they pay interest on that debt. However, the yield on the 10-year Treasury notes increased from the end of the first quarter of 4.2% to over 4.5% overnight. The yield on the 10-year has slowly come back down to around 4.3% at the end of the second quarter. For now, the markets are back up, and markets are pricing in hopes that countries negotiate favorable terms. The 90-day extension ended July 9th, however the administration has announced additional changes to the timeline to come to a trade deal.

Throughout the second quarter we continued to monitor the heavyweight fight over interest rates. The Federal Open Market Committee (FOMC) has a long-stated inflation goal of 2%. With inflation running in excess of 2% and FOMC members actively debating the long-term impact of potential tariffs, the Federal Open Market Committee has remained on hold and not lowered interest rates since the recent presidential election. The Administration would like the FOMC to lower short-term rates and at times has called for Federal Reserve Chairman Jerome Powell to step-down. The idea of firing Powell is not likely as it is an independent position but rumors of naming his successor early and creating a shadow Fed Chairman has been in the news. For now, we will follow Powell and his comments. Depending on what happens with tariffs, the Federal Reserve could cut rates one or two times in the Fall. For now, inflation is around 2.8%, higher than that stated goal of 2%.

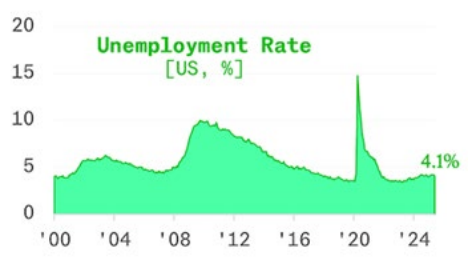

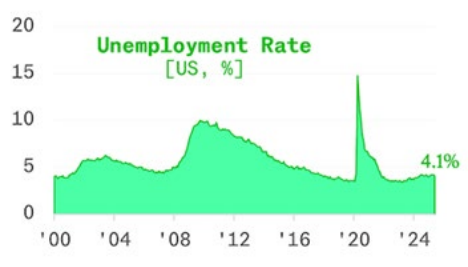

Another factor the Federal Reserve considers when determining interest rate policy is unemployment, which for now seems under control with more new jobs being added, 174,000 in June, and the unemployment staying at 4.1%.

While there is no shortage of things to be concerned about, the markets have looked at any selloffs or dips as buying opportunities. We are still monitoring the war between Russia and Ukraine and how the U.S. is involved. The same goes for Iran and Israel and the role the U.S. partakes in the Middle East as conflicting reports over Iran’s nuclear status remains unclear. Higher oil prices, resumption of student loan payments and higher long-term interest rates all influence the economy. The first week of the second quarter we had Liberation Day, and the first week of the third quarter we had the passing of a massive 900-page bill. The bill we be a theme during the third quarter and estimates of the increase on the federal deficit will be debated. We also had the last of the major rating agencies, Moody’s, downgrade the U.S. Treasury credit rating from Aaa to Aa1.

As we mentioned last quarter, we are long-term optimistic on the markets and look at any disruptions as opportunities. The use of structured notes can add a layer of downside protection for clients who are concerned. The notes can also help increase the income generated by your investment portfolios. Private equity and private credit add additional buffers from the volatility from public markets.

Our website and YouTube channel offer a wealth of information. You can find our videos through our website at: https://www.paragoncap.com/quarterly-market-insights

or on our YouTube channel. If you subscribe to our YouTube channel by hitting the “subscribe” button, you will be notified when new videos are posted.

In addition, for up-to-date news and thoughts from Paragon, plus interesting articles on current topics, we encourage you to follow us on LinkedIn and/or Facebook (links below). We have company pages for both and appreciate your liking and/or following us.

Also, please share your experiences with friends and family; we love the opportunity to help those you know with their financial success.

Whether you feel as if you’ve outgrown your advisor or you just want a fresh perspective on portfolio strategies in our current market, our team of experts is here for you.